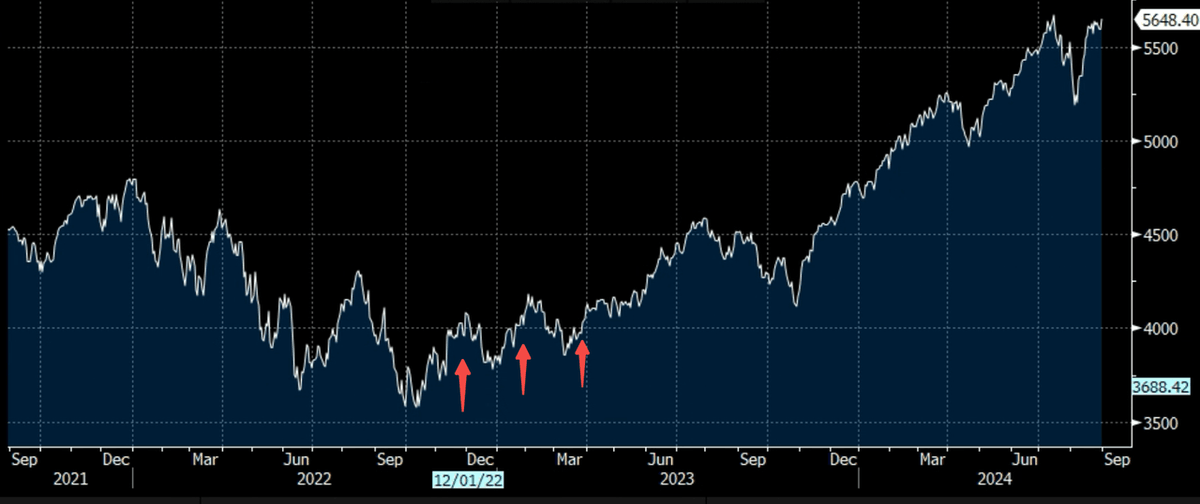

Model-Driven Rationality Outperforms Emotional Bias

The model issued bottom-fishing signals following two major US equity drawdowns in recent years:

- Case 1: In April 2020, after the COVID-driven crash, the model signaled bullish on the S&P 500 just as markets stabilized—avoiding panic and identifying the rebound early.

- Case 2: In late 2022, amidst negative sentiment from Fed rate hikes, the model repeatedly issued overweight signals on the S&P 500, capturing the next leg of the rally.